This is part of a series of posts about Storage Field Day 9.

Intel are a public company, so let’s use their SEC filings to find out what they’re up to.

Here’s my summary of Intel in one chart:

Intel segment sales (Source: SEC filings, eigenmagic analysis)

Intel is making less of its money from PCs (desktops and laptops) than it used to. There’s been a steady increase in revenue for the Data Center Group, driven mostly by cloud computing, according to the company’s 10-K filings.

The Internet of Things group is a new one. Intel change their divisional groupings from time to time, and IoT appears to have come into being in fiscal 2013, and it’s a pretty smart thing for Intel to get involved in, because the sensor market is very large, sensors are getting more computerised (rather than using special purpose micro-controllers) and ARM has a pretty good handle on that market already. Intel is playing catch-up there, in many ways, so it’ll be interesting to see how that plays out in future years.

The costs for these groups are interesting as well:

Intel cost of sales as % of sales category. (Source: SEC filings, eigenmagic analysis)

Margins on data center are better than everything else, and Software and Services has only just started having a positive profit contribution in the past three years. It’s helpful for Intel’s profits if they can can transition away from the higher-cost PC and laptop business as its growth declines.

We can also see that Intel is investing heavily in new technologies:

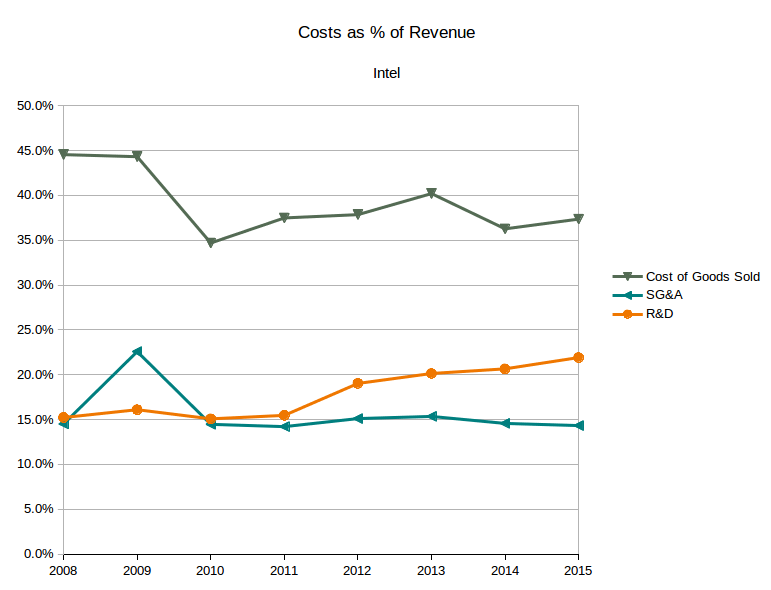

Intel costs as % of revenue (Source: SEC filings, eigenmagic analysis)

Sales and Marketing, and General and Administration (SG&A) costs are flat, and COGS is much improved from 2009, which is more a reflection of Intel winning the CPU war against AMD rather than Intel bringing per-unit costs down dramatically. From Intel’s SEC filings, the management commentary is that prices are staying high, so Intel isn’t being forced to drop the price of their processors to beat lower-priced competitors. People are happy to pay a premium for Intel’s products, so as a % of sales, the COGS looks lower.

And note the substantial increase in R&D expense (as % of revenue) while this has been happening to revenues:

Intel revenue, net profit, and gap between revenue and profit.

This shows that Intel has been investing a lot of money into R&D in the past 4-5 years, which has gone into things like 14nm fabrication capabilities, 3DXPoint memory (when we finally get to find out what it can really do) and NVMe.

Data Center tech is what we’re most likely to be looking at from Intel for SFD9, and while I’d love for Intel to let us in on what makes 3DXPoint go, they’re not likely to spill the beans on the magic material they’re using at a Tech Field Day event. I’d love to be wrong folks!

I expect we’ll get some stuff on 3DXpoint that will be without much in the way of new detail, but hopefully some interesting stuff on what’s coming with storage interconnection architectures.

We got a good taste of what we are likely to expect at Storage Field Day 8, but there was also this presentation at Virtualisation Field Day 4 that went a little broader and talks about data services. I hope we get something a bit newer, rather than just a re-run of Storage Field Day 8.

With so much money being spent on R&D, I hope Intel have some more stuff that’s ready to be unleashed on the world that they can tell us about.